Home to more than 127 million people, Japan is a regional corporate and financial hub, and one of the fastest evolving digital markets in the world: thirteen Japanese companies figured on this year’s Thomson Reuters 100 world-leading technology company list.

As our readers will know, such a society needs a robust digital infrastructure.

Japan has a notoriously insular approach to business and digital service provisioning, while its real estate prices and energy costs are among the highest on the planet; there is also a shortage of leasable dark fiber. The collection of islands is subject to frequent cataclysmic natural disasters that - as we have witnessed with horror in recent weeks - all too often ravage its cities.

How does one navigate the data center landscape in such a seemingly adverse environment?

In an attempt to answer this question, we spoke to Jabez Tan, head of research for the data center and cloud market at Structure Research, a Canadian market analysis provider specializing in digital infrastructure.

All in one

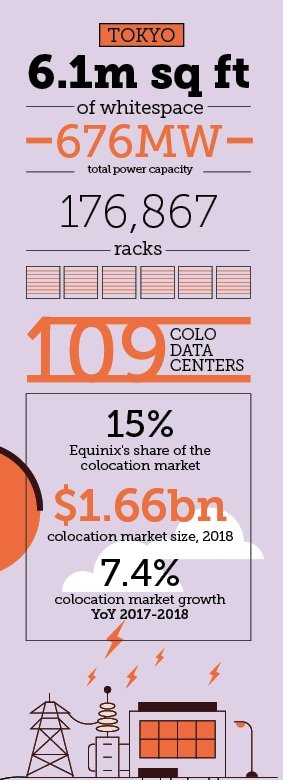

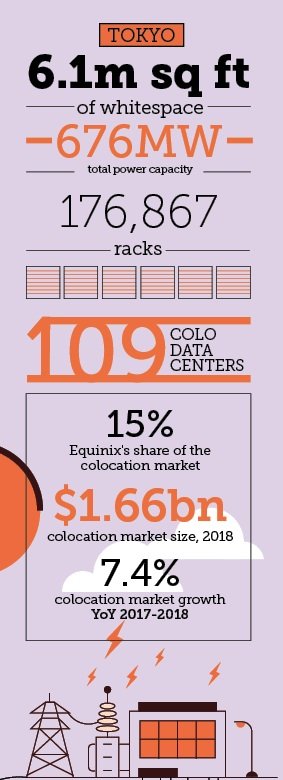

Structure recently published an analysis of the data center markets in, where most of the country’s activity is concentrated.

The Japanese data center market is unique in that it has traditionally been dominated by systems integrators like Fujitsu, Hitachi, Mitsubishi Electric and NEC.

These giants exist because Japanese companies want a “one-stop shop for their IT services,” preferring a single vendor with a broad portfolio to having to provision each service individually.

Systems integrators have been safe from foreign competition because, until recently, language and cultural barriers stood in the way of exchanges between international and domestic companies.

And until cloud providers began dominating the data center service industry globally, they had no incentive to change, explained Quy Nguyen, VP for global accounts and solutions at Colt DCS - a service provider which broke into the Japanese market in 2014, through the acquisition of local colocation and dark fiber provider KVH: “Many of them were making their money hosting private solutions; it’s a highly profitable business.”

But resting on their laurels is no longer an option; change is afoot. As the market matures, companies are becoming “more savvy and more educated in the way they deploy IT architectures and the way they procure IT,” Tan said.

They will perhaps learn from the massive colocation player Equinix - another foreign company which now brings in more than 15 percent of all of Tokyo’s colocation revenue, and is in the process of building a $70 million data center in the city, its eleventh in the Japanese capital.

With a mix of colocation, public cloud, and interconnection services in its facilities, Equinix allows customers to define their needs on a seasonal basis, offering more flexibility than any system integrator could.

Tan believes this will force some of the traditional local players to adapt and start offering more managed cloud services to their customers.

NTT, for example, recently merged its Dimension Data and NTT Communications subsidiaries, precisely to “form a more targeted entity to go after this kind of cloud opportunity,” he said.

For Nguyen, reluctance to change is part of Japan’s cultural fabric, and doesn’t necessarily mean that the local market won’t catch up with its international counterparts in due course.

“Japan has always been this way. They’re sometimes slow to jump on a trend, but once they do, it’s like a herd mentality.”

And, he ventured, “I think that’s what we’re seeing now: There’s no more perceived negativity on cloud services, security issues and such have been addressed and all the barriers have been removed.”

Others, like Digital Realty, have found their success not through acquisitions, but by teaming up with systems integrators: The colocation giant’s $1.8bn joint venture with Mitsubishi, MC Digital Realty, already accounts for more than three percent of Tokyo’s colocation market and seven percent of Osaka’s, in terms of IT load capacity. Promising to bring at least ten new data centers online, both of the venture’s participants stand to gain a lot from the country’s booming data center market.

Sturdy infrastructure

Another thing that makes Japan’s data center landscape stand out is that facilities here must be built to endure typhoons, earthquakes, tsunamis and tropical storms.

Somewhat counterintuitively, the high likelihood of natural disasters has not dissuaded companies from entering the market, and was identified by Structure as having an encouraging effect: after the 2011 disaster, companies anxious to ensure their own business continuity caused a spike in demand for local data center services.

And, because the country is prone to seismic activity, developers simply build Japanese data centers to withstand the worst weather conditions.

According to Tan, typically, in the basement of all data center buildings, “they’ll show you this giant seismic rubber contraption that acts like a spring so that when an earthquake hits, the building moves; instead of crumbling and breaking, at a certain level of vibration it rotates with the seismic activity.”

When it comes to the seismic isolation of a facility, Nguyen said, choosing the right systems isn’t complex, but more a matter of how much you are willing to invest.

Site selection based on strong bedrock is key, he explained, because “fundamentally, you can’t change the foundation that it sits on.”

This was the basis of Colt’s decision to build Inzai, which boasts a so-called probable maximum load percentage - the likelihood of a catastrophic failure in the event of an earthquake - of two percent. The company was vindicated in the 2011 earthquake, when the site experienced “no downtime whatsoever.” New players have all eyed neighboring sites, he said.

Real estate costs and a difficulty to access power due to tight government regulation of the energy sector have done little to dampen colocation providers’ zeal, either. And, because the market is at a turning point, only just opening its doors to international companies, it seems to have a lot of potential.

A new dawn

While the market is complex, for Tan it also holds great promise: from its status as a financial capital to its highly developed Internet economy, there is scope for growth in the Japanese data center industry. “I think there are a lot of drivers converging to make the Japanese market a lot more of an international powerhouse than it previously was.”

It would seem that Colt agrees. With a third Tokyo campus on the way, on which it is planning to break ground in the second quarter of 2019, Nguyen said: “I can’t disclose the exact figure, but my expectation is that before we go live with that site, we will be largely sold out.”

Of the six to ten interested parties, he said, it would take three to fill it to capacity.

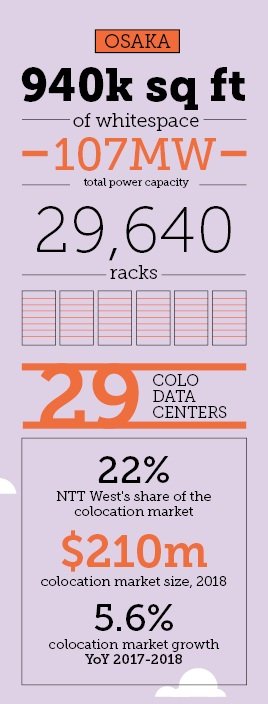

The company is also looking at building in Osaka, Japan’s second biggest data center market, where it currently leases a small amount of space in a third-party data center. It is worth noting that AWS, Google Cloud and Azure all have footprints in the city, too.

However, Nguyen added, “it is enormously difficult to find good land” there, and the company has passed on several opportunities which it considered substandard.

Analysts agree that international businesses will keep pouring into the country, especially in light of the upcoming 2020 Olympics, which Tan said will likely “drive a lot of analytics, big data, AI type workloads, supported by a lot of the media, digital media content and streaming platforms” that want to have local capacity ready for the games.

Nguyen noted that Colt has already received interest from new customers, a large portion of which come from China, representing viewing and payment platforms “and a lot of fintech solutions.”

The market’s newfound success has had a cumulative effect, he added, increasing demand on top of the hyperscale companies “from other US providers that previously had not had a big position in Japan.”

As well as driving more demand, the data center market’s growth could drive institutional change as well: the country may wish to reconsider its data sovereignty laws.

Compared to other regional markets, like China, Japan has not felt the need for data sovereignty, as its exchanges were most often domestically focused. Companies previously chose to host their core compute in Japan, but the decision was mostly latency-related.

For Colt, storing data locally is a nascent concern. Europe’s GDPR affects companies all around the world by governing where European data is processed, Nguyen said, but China’s flourishing fintech market rules have had a bigger effect locally: “Various Chinese entities each have their own payment scheme which they need to deploy locally for FSA purposes,” he said.

Whatever the future brings, one thing is certain: Japan, in all its uniqueness, is no longer an inward-looking, domestically-ruled market, but, much to the joy of its new entrants, a vast land of opportunity.

This article featured in the October/November issue of DCD>Magazine. For more information, or if you'd like to subscribe, click here or fill in the form below:

{kind=link}

{kind=link}

{kind=link}