How does the data center industry satisfy cloud providers at the same time as small colocation customers? It’s a crucial question for colocation providers. But is a $100 billion Japanese telecoms giant really the organization most likely to come up with the answer?

Those were our main questions for Doug Adams, CEO of RagingWire, when we met him at the company’s 28.4MW campus in Ashburn, Northern Virginia in 2018. He’s in a position to answer both. He helped found RagingWire in 2000, and has had nearly 20 years building and running colocation data centers for enterprises. For the past five years of this, RagingWire has been under the ownership of Japanese telco NTT, moving the company up to a new league.

For some, it would be a surprise to see a telecoms company buying into data centers. Most operators, from AT&T to Verizon, have cut back or got out of data center ownership altogether since 2015, leaving the business to specialists. Why does NTT think it can do better, and why buy RagingWire?

This feature appeared in the April issue of DCD Magazine. Subscribe for free today.

Life under NTT

Adams tells me the company started out without venture funding, providing space for business customers in California, and building a reputation for reliability. When telcos started realizing they couldn’t compete with the specialists, NTT took a longer view, and bought 80 percent of RagingWire in 2014, completing the purchase in 2017.

“[The US telcos] were very short-sighted, very quarterly focused,” he said. “They were getting their tushes handed to them by the Equinixes, Digitals and RagingWires of the world, and they backed out. I think NTT was extraordinarily intelligent for doubling down on this business.”

The company has data centers in 21 countries, mostly through acquiring providers such as RagingWire, along with NetMagic (2018) in India, Gyron (2012) in the UK, e-Shelter (2015) in Germany.

Most have kept their own branding locally, but centrally, they are all marketed under the NexCenter brand - which also includes a measure of standardization of the product. Adams meets regularly with the heads of e-Shelter and NetMagic, and: “We don’t use the same gensets, but we offer the same SLAs. We have a common set of APIs.”

It’s an arrangement that has a lot of advantages, said Adams, although it lacks the tax benefits of being a data center real estate investment trust (REIT) like Digital Realty or Equinix. “REITs are not the perfect answer,” he said, suggesting that REITs are limited in the services they can offer, and have to be structured as a set of national LLC companies, with regional variations. “NTT is a large non-REIT option, not constrained to the issues REITs have to deal with.”

There’s no doubt the US is important to NTT. It makes up 43 percent of global sales for data centers, and the top four markets represent 24 percent of global sales: “All of Europe is 19 percent, but Chicago, Texas, Silicon Valley and Northern Virginia together make up 24 percent of the globe.”

Adams is visibly excited to have such solid backing. He’s going after business from the cloud giants now, and he showed DCD the fruits of this in Ashburn, the largest data center hub in the US.

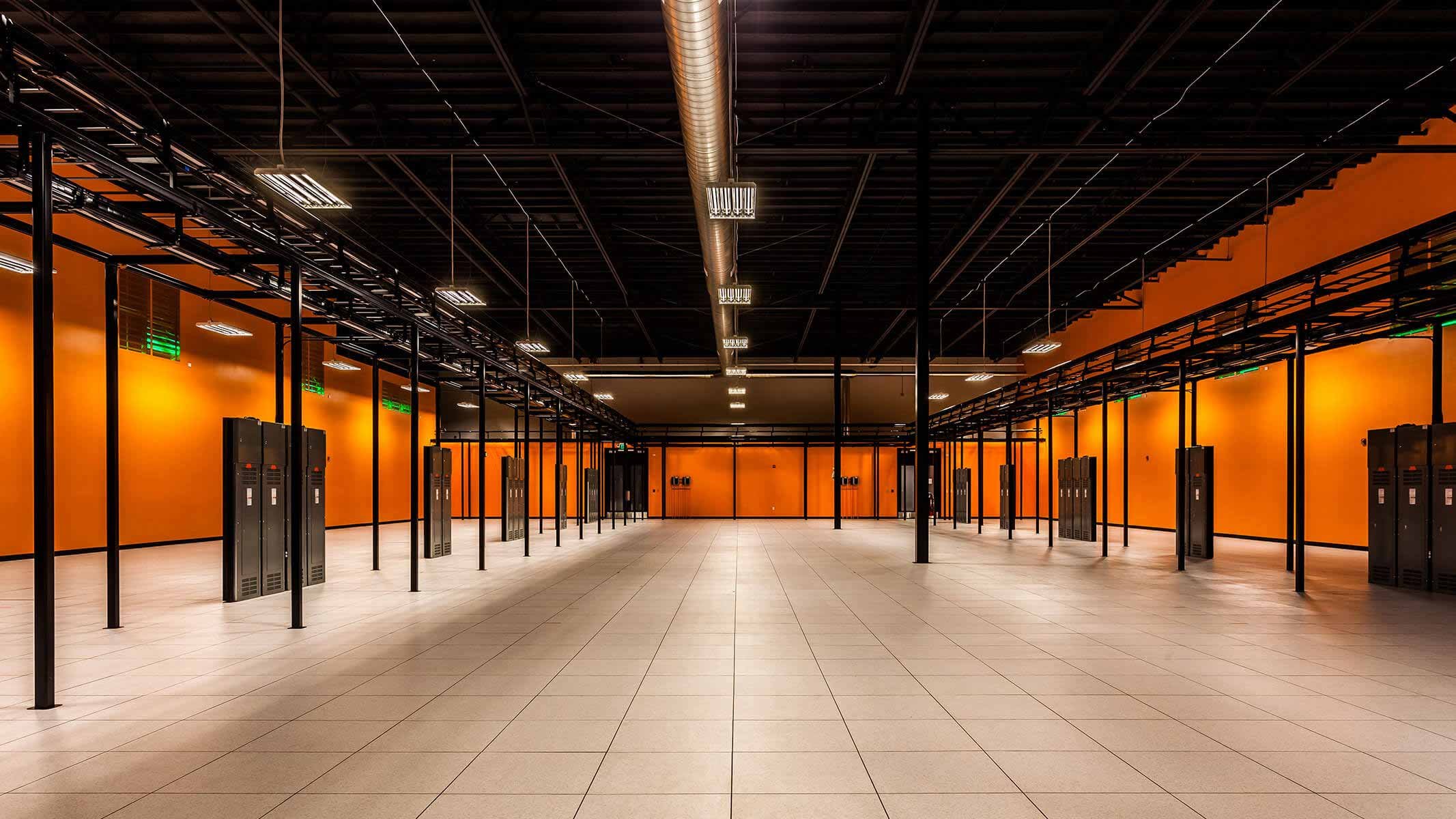

We met him in VA1, RagingWire’s first facility in Ashburn’s so-called Data Center Alley. It sits on a 78 acre plot where subsequent builds show the rapid pace of data center construction, and a change in RagingWire’s approach.

There are two other completed buildings, another two in construction, and space for eight in total. The three existing data centers are single-story: VA1 has a capacity of 14.4MW, VA2 has 14MW, and VA3 is a 16MW building. VA4 and VA5 are being built and pre-sold now, and both will be two-story 32MW facilities.

“There’s nothing stopping us,” said Adams. “We are doing pre-construction for VA5 at the same time as construction of VA4, because our funnel is strong enough we’ve already pre-sold part of VA4. When we’ve built VA4 by August 2019, we would expect much of it to be sold.”

The focus has shifted while the campus is being built. VA1 and VA2 were essentially stick-built, but the later buildings have become more modular: “VA5 will be the RagingWire 2.0 showcase.”

RagingWire now uses a prefabricated shell, and the space is sold while the concrete dries. The company prepares the site, including fiber pipes and power, and orders the shell. “Then we have it sitting on the lot of the pre-fabricator, and we go out and start pre-selling it,” said Adams. “The building is fit up and dried out in less than two months.”

This cycle gives the company a head start on selling, and it also allows for faster and cheaper construction, by shifting the building process away from winter: “We construct in a time when it is less expensive. We avoid the middle of winter, when there is snow, mud and rain.”

{kind=link}

{kind=link}

What the giants want

It’s also more focused on the needs of hyperscale customers for large capacity delivered fast and cheaply. VA1 and VA2 were made with 2MW vaults available, while VA4 and VA5 are offer 8MW halls.

On cost, Adams reckoned he can build for $7.5 million per megawatt. If others claim to manage $5 million per MW, they are stretching the truth he says, by leaving out things like land costs.

“This is a highly deceptive market when people frame up their actual build costs,” he told DCD. “People say anywhere from $5m to $10m, but if they are honest and building at scale, the price will be $7m to $8 million.”

The company still caters for smaller customers, however: “I can swing into the supergranular. We sell an 8MW hall, but we also do a 250kW break,” said Adams. “About 70 to 80 percent of our customers are wholesale, about 20 to 30 are more traditional retail.”

The combination actually has synergies: the building benefits from the economies of scale demanded by webscale customers, while the retail customers have the benefits of being close to those cloud providers: “It makes for a unique mix of customers. We’re not just retail, we’re not just hyperscale. We have the best of both. Retail equates to shorter terms and higher margins, while wholesale equates to longer terms and lower margins.”

It’s striking that the first Virginia facility, where we are, must have cost substantially more than the later price-competitive modular builds. RagingWire was a runner up in DCD’s Most Beautiful Data Center award in 2017 with its TX1 facility; the VA1 data center has the same attention to detail. It won a design award from Loudoun County’s Design Cabinet, praised for its “vibrant blue, yellow and purple exterior colors” and its “majestic, two-story atrium” with natural light.

“I think we consciously put a lot of amenities in the first building on the campus,” said Adams. “We try to make sure one building on each campus is a nice building, with all the bells and whistles. Thereafter, they are much more utilitarian.”

VA1 has office space, a games room, and carefully constructed observation windows, so visitors can see into the critical facilities space, without having to enter a secure area - a feature RagingWire has used in other sites including Sacramento’s SA3 facility.

I asked about a stretch of water by the facility. Other Ashburn operators refer to it as “The Moat,” implying it’s a sign of over-spending. Adams grinned at the suggestion: “Nah, it’s a retention pond.”

Compared to subsequent buildings, it is as if VA1 was “dipped in gold,” Adams laughed. Future buildings will be more of a “market standard,” but they will never the same as the rest: “In my opinion we are always going to build a better, higher quality data center. We don’t shoot for the de minimus level. I think we build within a stone’s throw of the super low cost providers, but we also add more value.”

There’s a distinctive atmosphere in Ashburn. All the operators are competitors, but they’re also friends; any critiques of each others’ products are good-natured, amounting to teasing.

Adams has an answer to that: “The reason we all talk to each other is, we are still in the second innings.”

He’s referring to baseball. Early in the match, people don’t take it so seriously: “In the third innings, we are all going to get a little upset with each other, because we are fighting over the same deals.

"In the fourth innings, we are all going to hate each other - but we are nowhere near the fourth innings.”