{kind=link}

According to the latest release of 451 Research’s Datacenter KnowledgeBase the global colocation market has surpassed a run rate of $25bn in revenue with six percent of datacenter firms accounting for more than half of global revenue. The figures are included in the latest release of their Datacenter KnowledgeBase (DCKB).

Data from the 451 Research’s DCKB reveals a pattern of market concentration with firms at the top with a long tail of firms at the bottom of the global colocation market. The top 10 players account for 28 percent of the $25bn in revenue and the top 60 players account for 52 percent of the $25bn in revenue. Despite a spate of merger and acquisition activity in the sector more than 1,000 additional companies, many of them strong regional players, generate the remaining 48% of revenue.

“At its heart, the multi-tenant datacenter business is a regional business,” said Greg Zwakman, 451 Research Director, Quantitative Services. “So despite active consolidation and some concentration at the top, much of the market remains highly fragmented, with a mix of national and local players”, he said.

According to 451 Research, over the past 10 years, much of the investment to build multi-tenant datacenters has been made in large markets where there are many potential tenants. “We are seeing growing interest in markets outside of those top few cities, however” said Kelly Morgan, 451 Research Director for Multi-tenant Datacenters in North America. “This is for several reasons, such as to reduce latency, to target medium-sized local businesses, or because operating costs are lower. We expect to see strong growth in several of these secondary markets over the next few years.”

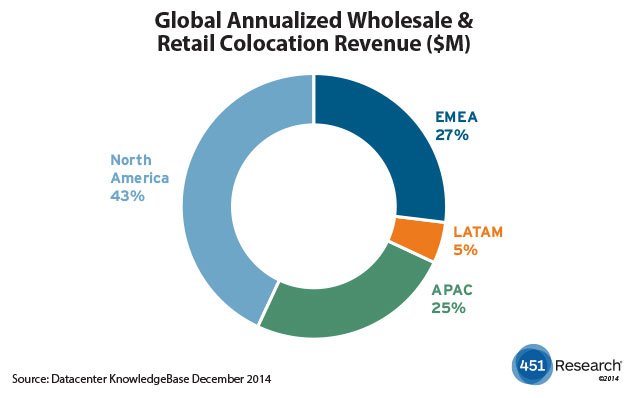

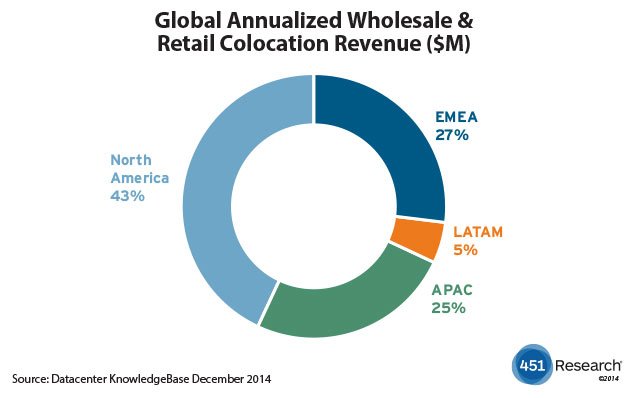

DCKB data also details 176 known facility expansions and 134 new builds globally, with key regions such as New York City and London leading in square footage/power coming online over the next couple of years. Currently, a little over 60 percent of planned expansions and new builds are concentrated in North America, but APAC and EMEA are both posting strong expansion rates as well and we are actively researching those areas to determine where additional builds/expansions are likely. LATAM data centers are increasingly catching up to their counterparts in other regions in terms of average revenue per facility, representing 4.5% of the 3,685 datacenters tracked by the DCKB and 5% of global sales (see today’s feature on Columbia – ed).

The DCKB database covers 3,685 individual datacenters from 1,086 datacenter companies serving North America, EMEA, APAC and LATAM. 451 Research is a preeminent information technology research and advisory company with a core focus on technology innovation and market disruption.

https://451research.com/